By Bassam Zaazaa – arabnews.com — BEIRUT: A Lebanese man was released on bail this week after a fortnight in detention for taking people hostage and threatening to blow a bank up while trying to withdraw $50,000 of his own money. Abdullah Al-Saii armed himself with a gun, grenade and bottles of benzene before entering […]

![]()

by arabnews.com — Najia Houssari — BEIRUT: In anticipation of US Envoy for Energy Affairs Amos Hochstein’s expected visit to Lebanon next week to discuss maritime border demarcation, Lebanon sent a letter to the UN “to shift negotiations on the southern maritime border from Line 23 to Line 29, while retaining the right to amend Decree No. 6433 in the event of reluctance and failure to reach a fair solution.” The letter explicitly states that “the area between lines 1 and 23 to the area between lines 23 and 29, with an increase of 1,430 square km in addition to the previous 860 square km, is the disputed area, including the Karish gas field.” In this letter, Lebanon does not abide by the “oil field in exchange for an oil field” negotiation principle, i.e. the Qana field in favor of Lebanon versus the Karish field for Israel. Rather, it includes a clear indication that the Karish field “is a disputed area, and Israel cannot continue its exploration operations nor begin extraction operations.”

Lebanon’s letter stresses that “the Israeli action in that disputed area endangers international peace and security.” This development is considered an escalation by Lebanon to speed up indirect negotiations with Israel, which are being handled by the US under UN auspices. The letter, addressed under the guidance of President Michel Aoun to the president of the Security Council on Jan. 28 and whose contents were just made public, stipulates that Lebanon adheres to its right to an area of 2,290 square km and not 860 square km only. A political observer told Arab News that Aoun had sent the letter to the government but did not receive a response approving or objecting to it. “The letter included a veiled threat aimed at accelerating negotiations and making achievements before Aoun’s mandate ends, and perhaps opening closed political doors for his son-in-law, MP Gebran Bassil, to recommend him as his successor,” the observer said. The letter read: “Out of respect for the principle of the ‘negotiating path’ that was not reached after the indirect negotiations, one cannot claim that there is a proven Israeli exclusive economic zone, contrary to what the Israeli side claimed regarding the so-called Karish field.”

*بيان صحفي لمجلس الأمن حول لبنان* https://alhadeel.net/article/323037/ البيان يطالب لبنان التقيد باعلان بعبدا للاطلاع ان البيان الصحفي في مجلس الامن يتطلب موافقة ١٥ عضو على ١٥ او ١٤ موافق وواحد نأي بالنفس عن التصويت او ١٣ موافق و٢ نأي بالنفس. اذا احد الاعضاء رفض نص البيان فلا يمكن اصداره

One year after the murder of Lokman Slim, a Lebanese journalist and political analyst who had been threatened by Hezbollah activists for months, Reporters Without Borders (RSF) has referred the decline in the security of journalists in Lebanon to the UN and has asked it to ensure that the authorities take all necessary measure to protect them and guarantee their safety. Slim was found dead near his car exactly one year ago, on 4 February 2021, after setting off for his home in Beirut. Despite the many reasons for suspecting Hezbollah members, who had threatened him for months because of his criticisms, the investigation never got any leads on the identity of his killers in order to bring them to justice.

RSF therefore formally referred Slim’s murder, and the cases of 27 other journalists who have been the victims of serious threats or acts of violence, to the United Nations at the end of January, in order to sound the alarm about the disturbing decline in press freedom and journalists’ safety in Lebanon since October 2019. In its “allegation letter” to the three UN Human Rights Council special rapporteurs on extrajudicial executions, freedom of expression and violence against women, RSF urges the UN to press the Lebanese authorities to guarantee the safety and protection of journalists, whose working environment has declined sharply since the start of anti-corruption protests in October 2019 and the Beirut port explosion in August 2020. “Independent, impartial and thorough investigations must be carried out into all acts of violence and crimes against journalists,” said RSF advocacy director Antoine Bernard. “Journalists are paying a high price for the culture of impunity that prevails in Lebanon. It is essential that those responsible for these crimes are identified, prosecuted and convicted.”

By Najia Houssari — arabnews.com — BEIRUT: Hospital emergency departments have been mired in violence and a dentist was killed in his clinic in a week that saw violent crime rise in Lebanon. Violence has not been limited to medical workers, with a child kidnapped from his mother and organized armed gangs running riot in various regions. The Syndicate of Hospitals in Lebanon said it fears that hospitals could become a “punching bag” for a frustrated populace struggling through the economic crisis. Doctors have claimed that several of the security incidents relate to rising hospital bills. Other incidents have seen Lebanese attempting to claim their rights by force, such as obtaining an unavailable bed in a hospital or claiming a cash deposit held by the bank.

Among the capital’s hospitals, Al-Makassed endures attacks on the medical, nursing and administrative staff more than any other, particularly in the emergency department. The hospital administration said a few days ago that the attacks were committed by “barbarians who are insulting, beating and threatening the ER doctors in an unexpected way.” The hospital has closed its ER until the medical body is provided with security. Less than 24 hours after a violent outbreak in the Beirut hospital, the same scenario took place in Sheikh Ragheb Hareb University Hospital in Nabatieh, where Hezbollah and the Amal Movement are extremely powerful. Vandals smashed up the ER department and medical staff were beaten while attempting to care for a patient. The cameras showed the parents of the patient and the nursing staff quarreling, which escalated into fighting, resulting in a number of injuries and the destruction of some medical equipment.

by EPHREM KOSSAIFY – arabnews.com — NEW YORK: The UN Security Council on Friday called on Lebanese political parties to distance themselves from external conflicts and instead focus on the urgent implementation of political and economic reforms that are needed to unlock international financial support and alleviate the “dire needs” of the Lebanese population. Members of the council, the most important body within the UN, urged Lebanese parties to implement “a tangible policy of disassociation from any external conflicts as an important priority, as spelled out in previous declarations, in particular the 2012 Baabda Declaration.” The Baabda Declaration was designed to underscore Lebanon’s neutral position with regard to events in the region.

The powerful Lebanese Shiite party Hezbollah, which serves as the strategic arm of the Iranian regime in the region, has been involved in the Syrian civil war, fighting alongside the Assad regime, and in Iran’s proxy wars in Yemen and Iraq. Council members welcomed a meeting of the Lebanese cabinet that took place on Jan. 24 but urged the authorities to quickly implement necessary reforms, including the adoption of a budget for 2022 that reflects previous agreements with the International Monetary Fund.

by devdiscourse.com — Lebanon received a letter from Luxembourg authorities asking for information relating to Lebanon Central Bank Chief Riad Salameh’s bank accounts and assets, a senior Lebanese judicial source confirmed to Reuters. The source did not elaborate. A spokesperson for Luxembourg’s judiciary confirmed to Reuters in November https://www.reuters.com/world/middle-east/luxembourg-judicial-authorities-open-criminal-case-related-lebanon-central-bank-2021-11-15 it had opened “a criminal case” […]

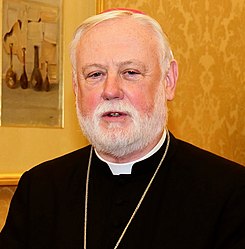

NNA – The Vatican’s Secretary for Relations with States, Archbishop Paul Gallagher, confirmed from the Grand Serail that he came to Lebanon carrying the message of His Holiness Pope Francis, “it is a message of hope for a country that means a lot to him, and we are here to support the Lebanese and to assure them that we stand by their side in the face of challenges, and the decision for Lebanon’s recovery is a purely Lebanese decision on which efforts must be combined.” Prime Minister, Najib Mikati, on Thursday welcomed at the Grand Serail Archbishop Gallagher, and an accompanying delegation. During the meeting, Premier Mikati welcomed Archbishop Gallagher, saying: “We are proud of the affinity that His Holiness Pope Francis expresses towards all the Lebanese, and shares their pain and suffering that has impacted most aspects of their lives.” Mikati added: “We appreciate your call for Lebanon to remain a project of peace and a homeland for tolerance and pluralism, where all sects and religions come together.”

The PM added, “We are persisting and determined to implement the government’s reform program despite all obstacles and difficulties, and we are all convinced, as you stated yesterday, that reforms are the ones to help Lebanon, along with the support of the international community.” Archbishop Gallagher, in turn, indicated: “Change is coming to Lebanon, and we pray that it will be for the good of this country, and in the name of His Holiness the Pope and the universal Catholic Church, we will always stand by Lebanon’s side.”

NNA – The following is US Ambassador Dorothy C. Shea’s address as delivered marking one year anniversary of the assassination of Lokman Slim:

“Let me begin by renewing my sincere condolences to the family of Lokman Slim as well as to all of those gathered here and beyond, who loved him, who worked with him. All of us here were affected by his work. Lokman stood for the rule of law. He was a champion of free speech, democracy, and civic participation. He was never intimidated by the repeated threats made against him. In his life, he fought for justice and accountability. In his death, he deserves those things. It is an extremely sad occasion for us all to mark the one-year anniversary of his assassination and it is even more troubling to see that there has yet to be justice. There has yet to be accountability.

كتب الرئيس العماد ميشال سليمان : لم نشكك لحظة واحدة بقدرة قوى الامن الداخليي وفرع المعلومات على تحرير الطفل المخطوف ليس فقط لكفاءة الجهاز الامني المشهودة وسرعة تحركه بل ايضاً لعدم تغطية المجرمين من قبل اي طرف. الحمد لله على سلامة الولد وعودته سالماً الى اهله والتحية الى قوى الامن وفرع المعلومات مع بالغ التقدير […]

سجعان قزي

@AzziSejean

اللبنانيّون من مختلفِ الطوائفِ مَعنيّون أخلاقيًّا وجُغرافيًّا بالصراعِ العربيِّ ــــ الفارسيِّ في الـمِنطقة، فهم يَنتمون إلى العالمِ العربيِّ. ومعنيّون أخلاقيًّا ووطنيًّا بالنزاعِ بين السُنّةِ والشيعةِ في لبنان، فهما مكوِّنان أساسيّان في الشراكةِ الوطنيّة. أنْ نكونَ معنيّين لا يُبرِّرُ مطلقًا الانحيازَ عسكريًّا إلى الصراعِ في المنطقةِ، ومذهبيًّا إلى النزاعِ في لبنان. وأنْ نكونَ حياديّين لا يَعني أن نساويَ بين مَن يساعدُ دولةَ لبنانَ وشعبَه في كلِّ المجالاتِ (دولُ الخليجِ العربيّةُ)، وبين مَن يواصِلُ الهيمنةَ على دولةِ لبنان والإساءةَ إلى شعبِه (إيران وحلفاؤها). وأنْ نكونَ حياديّين لا يَعني أيضًا أن نساويَ بين مَن التزمَ مشروعَ الدولةِ (غالِبيّةُ السُنّةِ)، وبين مَن يَلتزِمُ مشروعًا مناقِضًا الدولةَ (حزبُ الله).

ليس اللبنانيّون ضِدَّ إيران وحزبِ الله لأنهما شيعةٌ، وليسوا مع القِوى السنيّةِ الوطنيّةِ لأنّها سُنّية. الخِيارُ الوطنيُّ يُحدِّدُ الـمَعيّةَ بمنأى عن الانتماءِ الطائفيّ. أصلًا ليس الحيادُ الامتناعَ عن الدفاعِ عن النفسِ وعن استقلالِ كيانِ لبنان وسيادةِ دولتِه ومصالحِ شعبِه أكان المعتدي لبنانيًّا أو غريبًا. حدودُ الحيادِ هي حدودُ سيادةِ لبنان. وحدودُ السيادةِ ألّا يَعتديَ أحدٌ علينا وألّا نعتديَ على أحد.

في هذين الواقِعين اللبنانيِّ والإقليميِّ ينحازُ لبنانُ إلى ذاتِه. فلبنانُ، شعبًا ودولةً وكِيانًا ونِظامًا، يتعرّضُ اليومَ لحربٍ غيرِ معلَنةٍ، ولانقلابٍ من دونِ بَلاغات. تجاهَ هذه الحالات، تَستَسلمُ الشعوبُ أو تُقاوم. وحَسْبي أنَّ اللبنانيّين أهلُ مقاومة (وإنَّ الأمسَ لذاكِره قريب). لذلك لا حرجَ في اتّخاذِ موقِفٍ صريحٍ وشُجاعٍ لصَدِّ الحربِ ووقفِ الانقلاب هذا لا يَنتهِكُ مفهومَ الحياد. مؤسِفٌ أنْ يَفرِضَ علينا حزبُ الله وإيرانُ، رغمًا عنّا، هذا الموقفَ، فيما نَطمَحُ إلى أفضلِ صداقةٍ مع إيران وأحسنِ شراكةٍ مع جميعِ شيعةِ لبنان. يَزعَمُ حزبُ الله أنّه لا يُوجِّهُ سلاحَه نحو الداخل اللبنانيّ (!!!)، لكنَّ مواقفَه وتصاريحَه ضِدَّ شركائِه في الوطن وأصدقاءِ لبنان مؤذيةٌ أكثرَ من سلاحِه. السلاحُ يَقتلُ فردًا بينما الموقفُ يَقتلُ وطنًا.

Population Movements to Keserwan - The Khazens and The Maans

ما جاء عن الثورة في المقاطعة الكسروانية

ثورة أهالي كسروان على المشايخ الخوازنة وأسبابها

Origins of the "Prince of Maronite" Title

Growing diversity: the Khazin sheiks and the clergy in the first decades of the 18th century

Historical Members:

Barbar Beik El Khazen [English]

Patriach Toubia Kaiss El Khazen(Biography & Life Part1 Part2) (Arabic)

Patriach Youssef Dargham El Khazen (Cont'd)

Cheikh Bishara Jafal El Khazen

Patriarch Youssef Raji El Khazen

The Martyrs Cheikh Philippe & Cheikh Farid El Khazen

Cheikh Nawfal El Khazen (Consul De France)

Cheikh Hossun El Khazen (Consul De France)

Cheikh Abou-Nawfal El Khazen (Consul De France)

Cheikh Francis Abee Nader & his son Yousef

Cheikh Abou-Kanso El Khazen (Consul De France)

Cheikh Abou Nader El Khazen

Cheikh Chafic El Khazen

Cheikh Keserwan El Khazen

Cheikh Serhal El Khazen [English]

Cheikh Rafiq El Khazen [English]

Cheikh Hanna El Khazen

Cheikha Arzi El Khazen

Marie El Khazen