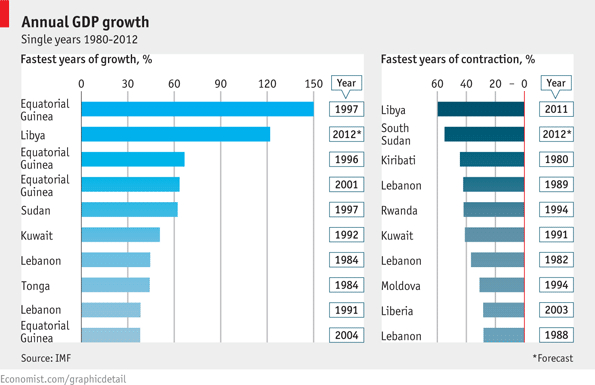

WHAT will be the fastest growing economy in 2012? The answer is perhaps surprising: Libya. It is projected to grow by an extraordinary 122% this year, according to the IMF, as oil production recovers faster than expected.

That is, however, only the second fastest year of growth in the IMF’s database (which stretches back over three decades).

The quickest was recorded by Equatorial Guinea, a country of 720,000 people on (and off) West Africa’s coast. Until the 1990s it was a dirt-poor country selling cocoa and timber. In 1996, it attracted heavy foreign investment in a recently discovered offshore oilfield (resulting in a current-account deficit of 125% of GDP). In the following year, the country produced 80,000 barrels per day of light crude, increasing its GDP by almost 150%.

In Equatorial Guinea’s case, fast growth followed a lucrative discovery. In most cases, though, it follows a nightmarish disaster.

Kuwait’s economy contracted by 41% during the Gulf War of 1991, before growing by over 50% in the subsequent year. Libya’s economy shrank by about 60% in 2011, as the country descended into civil war and foreign oil firms evacuated their staff. Sharp contractions set the stage for rebounds, both economically and statistically. They can create a lot of slack—unused capacity or unemployed workers—that can be swiftly exploited when the economy recovers. They also create a smaller “base”, from which subsequent growth is measured. If a country’s GDP shrinks by 60%, it must grow by 150% just to restore its former size.

Thus even if Libya fulfils the IMF’s forecast for this year, its GDP will still be smaller than it was in 2010.

Click here to subscribe to The Economist